Technological change is the realm of the Red Queen, and almost every product, every job, and every life is being increasingly touched by technological change. As a product to survive and stay relevant you must invest more in differentiation, marketing, and continuous improvement weekly. However this is increasingly no different for our careers where the time decay of specific skills can suddenly reach a tipping point forcing people with no intention of change to go into entirely new specializations, roles, even industries.

From Farnam Street’s “The Red Queen Effect”:

In Through the Looking Glass, Alice, a young girl, gets schooled by the Red Queen in an important life lesson that many of us fail to heed. Alice finds herself running faster and faster but staying in the same place.

Alice never could quite make out, in thinking it over afterwards, how it was that they began: all she remembers is, that they were running hand in hand, and the Queen went so fast that it was all she could do to keep up with her: and still the Queen kept crying ‘Faster! Faster!’ but Alice felt she could not go faster, though she had not breath left to say so.

The most curious part of the thing was, that the trees and the other things round them never changed their places at all: however fast they went, they never seemed to pass anything. ‘I wonder if all the things move along with us?’ thought poor puzzled Alice. And the Queen seemed to guess her thoughts, for she cried, ‘Faster! Don’t try to talk!’

Eventually, the Queen stops running and props Alice up against a tree, telling her to rest.

Alice looked round her in great surprise. ‘Why, I do believe we’ve been under this tree the whole time! Everything’s just as it was!’

‘Of course it is,’ said the Queen, ‘what would you have it?’

‘Well, in our country,’ said Alice, still panting a little, ‘you’d generally get to somewhere else — if you ran very fast for a long time, as we’ve been doing.’

‘A slow sort of country!’ said the Queen. ‘Now, here, you see, it takes all the running you can do, to keep in the same place.

If you want to get somewhere else, you must run at least twice as fast as that!’

Increasingly it seems the borders of slow sorts of countries are shrinking.

Jobs requiring education often evolve or are disrupted. Trades (plumbing, mechanics, electricians, carpentry) has proven resilient but even portions of these fields could be disrupted. Extremely high quality prefab homes are being built by startups driven to make housing affordable, fast to build, and more accessible. It seems like the loser in this transaction is the labor that went into the much slower conventional house.

Another example is mechanics, electric vehicles do not require oil changes, do not require replacement spark plugs, do not require transmission fluid changes, and do not require lubricants like ICE vehicles [1]. In fact hybrid and electric vehicles require ~3x less brake replacements as wear on pads, rotors, calipers is instead used to engage an electric motor and turn that lost momentum into electricity to recharge the vehicle [2]. This might result in fewer mechanics over time. This is before we factor in self driving and vertical integration of these hypothetical self driving car companies.

My world view has been biased by my own experiences.

My career hasn’t been conventional. Depending on how we define career I started in the less desirable areas of the service industry, replaced those jobs around 18 with freelancing in web design, then web development, then an emerging area now long taken for granted: mobile development. The latter was actually inspired by an article I read that impacted me so strongly me that I persuaded a few friends that we should incorporate a company to try to get into this mobile thing. I wish I could say we were a runaway success and retired early, this isn’t the type of story. We had the technical chops but not the business chops and ended up shutting down a few years later.

While working for myself or companies I founded I also interned every year I was in school. First as IT / web design for a small derivatives broker, also doing odd part time jobs including trying my hand at cold calls, and finally moving onto automated trading systems at the same firm. I also held a couple software engineering internships at a startup and a fortune 500.

All of the above before I had a degree.

At some point I ended up becoming a more stable salaried software engineer. Not knowing how the world works I didn’t move to a tech hub and joined a large well respected but shrinking tech company. There I experienced quarterly layoffs and watched many very smart and overly loyal people get pushed out of a company they spent their life building.

A few years later seeing the writing on the wall I was back into startups, this time at a fintech bringing the power of expensive financial terminals to the retail investor. Despite failing to raise money and shutting down after 6 months we made substantial progress and that led me to pivot into a new career, this time in a major tech hub: PM.

Back in a large company I worked harder than I ever worked to learn an entirely new job, and to be held to standards far higher than I ever had before.

Honestly it kicked my ass.

I learned a ton, and adapted, but within my individual team turnover was extremely high, and frankly everyone was fungible. We were all just one bad month from being replaced. I realized I really wasn’t getting a good return on investment for putting in 60-80 hour weeks, what I was doing (mainly project management at that point) was just too common of a skill set.

During college and before I was always very interested and involved in security, but I didn’t want to pigeon hole myself opting for being a generalist software engineer instead of a penetration tester or researcher. Now we were overhauling some areas of our product with a security focus and I took that as an opportunity to dive back in. My studying outside of work of course went far beyond the above and a couple months and maybe 50-100 cold emails later I’d be in the job I’ve had the past 5 years: Product Management with a security focus.

At the cost of less optionality and going deep into one or two specializations I found much more job stability, and a place to grow. The last ~5 years have in many ways been better than I could have imagined for what a job could be. As I reflect on what I want to do next my world is still wide open. I could focus on security and become an applied researcher, stick to product and work on some of the most challenging security and machine learning problems in the world, try to ride what I speculate will be the next big secular trend in tech (Web3), or as many readers of my blog might have gathered I could get involved in finance or fintech again.

I don’t know what I will do next but thus far taking risks and trying new things has at worse cost me some bruises, some time, or some money, but at best they’ve been radically life changing for the better.

We live in a world of rapid change that is both punishing and rewarding at times. The more popular a path is the more competition there is and this applies in your career, business, and life.

Looking at how the tech landscape has transformed during my career the spoils have gone to those willing to invest in human capital and research. As every company becomes a tech company this increasingly applies to all industries. As I’ve discussed before Clayton Christensen describes 3 types of innovation: Efficiency Innovation, Sustaining Innovation, and Disruptive Innovation.

What I experienced at my first job was efficiency innovation and sustaining innovation at a company that used to invest in disruptive innovation. Failure to stay efficient can lead to both a failure to attract investment and squeeze margins lowering the ability to invest in future product improvements or potentially disruptive new lines of business, but it is possible to be “too efficient”. Efficiency innovations around doing more with less works really well until it doesn’t, but from the perspective of Wallstreet it often looks great when reducing costs while ideally profits continue to grow. I find companies overly focused on efficiency often lose the plot of what is important going through down sizing, right sizing, re-organization, and re-structuring over and over in an effort to squeeze out another drop of profit from cost cutting. Worse case is when this is in a shrinking industry or market.

Sustaining innovation is the world of the Red Queen. If a car manufacturer doesn’t release a better car with comparable new and existing features to their competitors they are left behind. This is the default state of business. Simply to maintain existing market share you must continuously run faster just to stay in the same place. If you can offer a product better than the last that is cheaper or obviously differentiated from your competitors maybe you can even gain market share next year.

The investment in sustaining innovation is most essential the more alike you and your competitors are.

Over the years, we had the option of making large capital expenditures in the textile operation that would have allowed us to somewhat reduce variable costs. Each proposal to do so looked like an immediate winner. Measured by standard return-on- investment tests, in fact, these proposals usually promised greater economic benefits than would have resulted from comparable expenditures in our highly-profitable candy and newspaper businesses.

But the promised benefits from these textile investments were illusory. Many of our competitors, both domestic and foreign, were stepping up to the same kind of expenditures and, once enough companies did so, their reduced costs became the baseline for reduced prices industrywide. Viewed individually, each company’s capital investment decision appeared cost- effective and rational; viewed collectively, the decisions neutralized each other and were irrational (just as happens when each person watching a parade decides he can see a little better if he stands on tiptoes). After each round of investment, all the players had more money in the game and returns remained anemic.

Thus, we faced a miserable choice: huge capital investment would have helped to keep our textile business alive, but would have left us with terrible returns on ever-growing amounts of capital. After the investment, moreover, the foreign competition would still have retained a major, continuing advantage in labor costs. A refusal to invest, however, would make us increasingly non-competitive, even measured against domestic textile manufacturers.

His conclusion, emphasis mine:

My conclusion from my own experiences and from much observation of other businesses is that a good managerial record (measured by economic returns) is far more a function of what business boat you get into than it is of how effectively you row (though intelligence and effort help considerably, of course, in any business, good or bad). Some years ago I wrote: “When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.” Nothing has since changed my point of view on that matter. Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

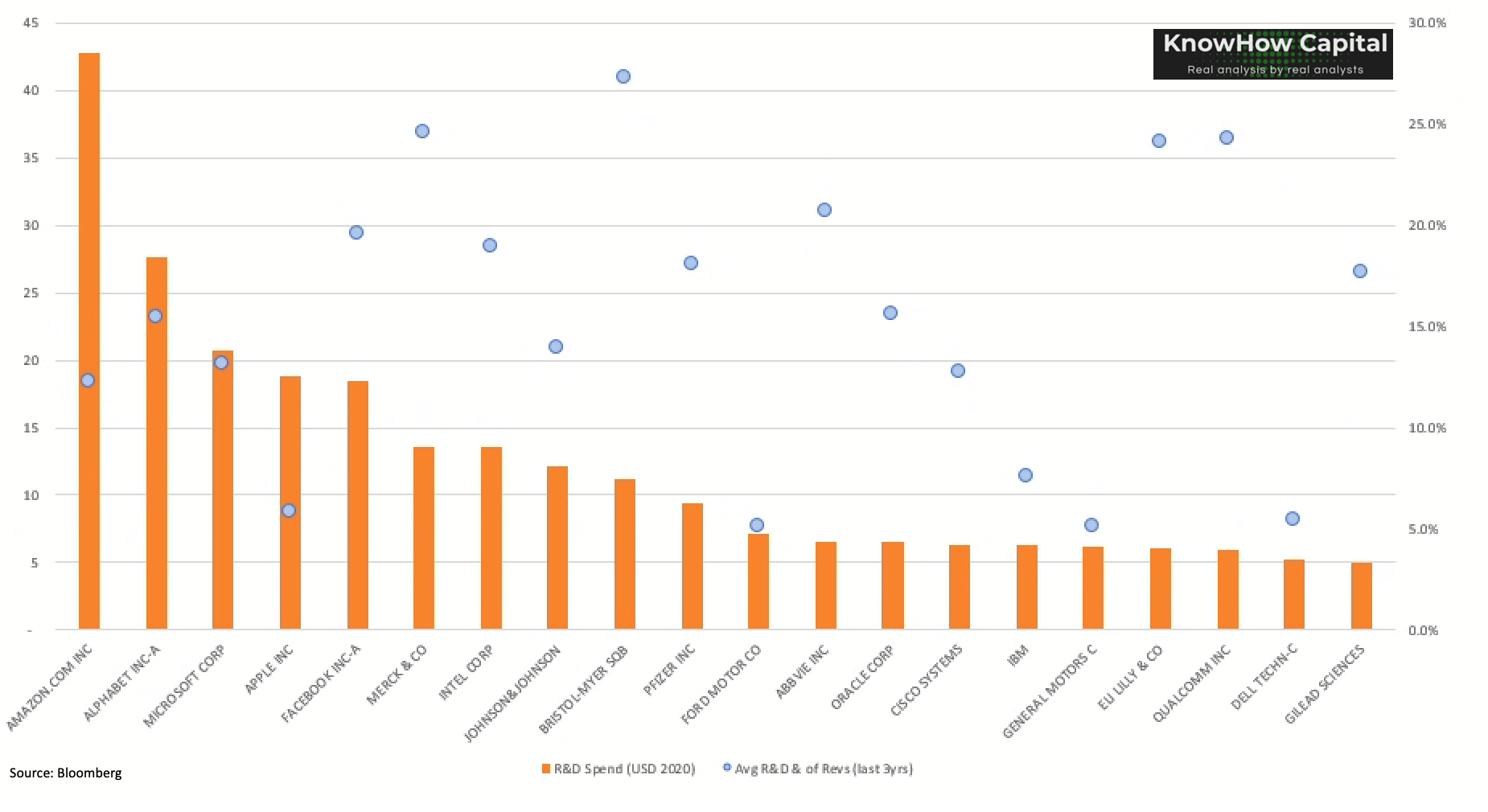

The above doesn’t mean not to invest, but to be wise or lucky on where to invest. If we look at the most successful companies of the last decade they invested considerable amounts into R&D and it appears to have paid off.

But simplistically, if you invest well and have a lot of money to invest, you will generate the most returns. No surprise then that the top r&d spenders in the US are also some of the best performing stocks of the past 10yrs.

…

Of course, as this chart from Strategy + Business shows, spending big doesn’t always lead to returns. Without embracing an innovative culture, it can just be money down the drain. Hence, make sure you bring your own qualitative overlay to the analysis we are about to run you through.

The most successful companies are swinging for the fences with new lines of business and attempts at disruptive innovations, improving their existing offerings with sustaining innovations, and investing in lean operations and efficiency improvements. Increasingly all 3 are required to be competitive if you’re competing with the best.

Tech is not a “slow sort of country” to quote the Red Queen. This came up with a discussion last month with Clueless on Amazon’s huge and ever increasing Capex and was the inspiration for this article:

Will they continue to make wise investments and find opportunities as good as their past opportunities? That is anyone’s guess, but companies that are highly innovative and willing to invest heavily are where I’ve been most successful as an employee and as an investor. Anecdotally I’ve seen the type of people who keep a beginners mind and try different things without a fear of failure have been the most successful. Trying more things and being willing to fail across many survivable bets seems to lead to a bigger “luck surface area” for those taking risks in business and in life.

Have you used the red queen mental model to improve your life, career, or investments? Feel free to share.