Link Roundup: July 2nd 2021

Geopolitics and Cyber, ML Compute, & Intangible Value Investing

Geopolitics and Cyber, Machine Learning Hardware, & Intangible Value Investing

Today I will be sharing some interesting content from other authors with a focus on:

The defense industry and geopolitics of cyber attacks

Innovations in hardware for machine learning computation

Intangible Value when Investing

If you find this content interesting or enjoyable please subscribe and share. That is my signal and motivator to produce more content more frequently.

The defense industry and geopolitics of cyber attacks

Quotations and graphics from Elad Gil’s Anduril Interviews

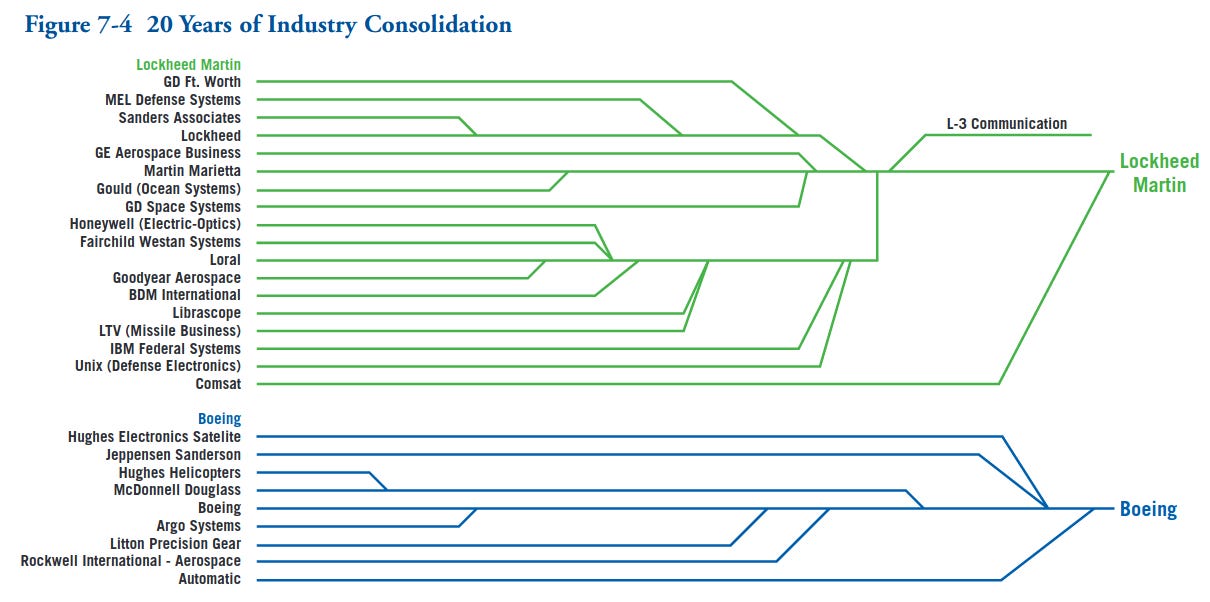

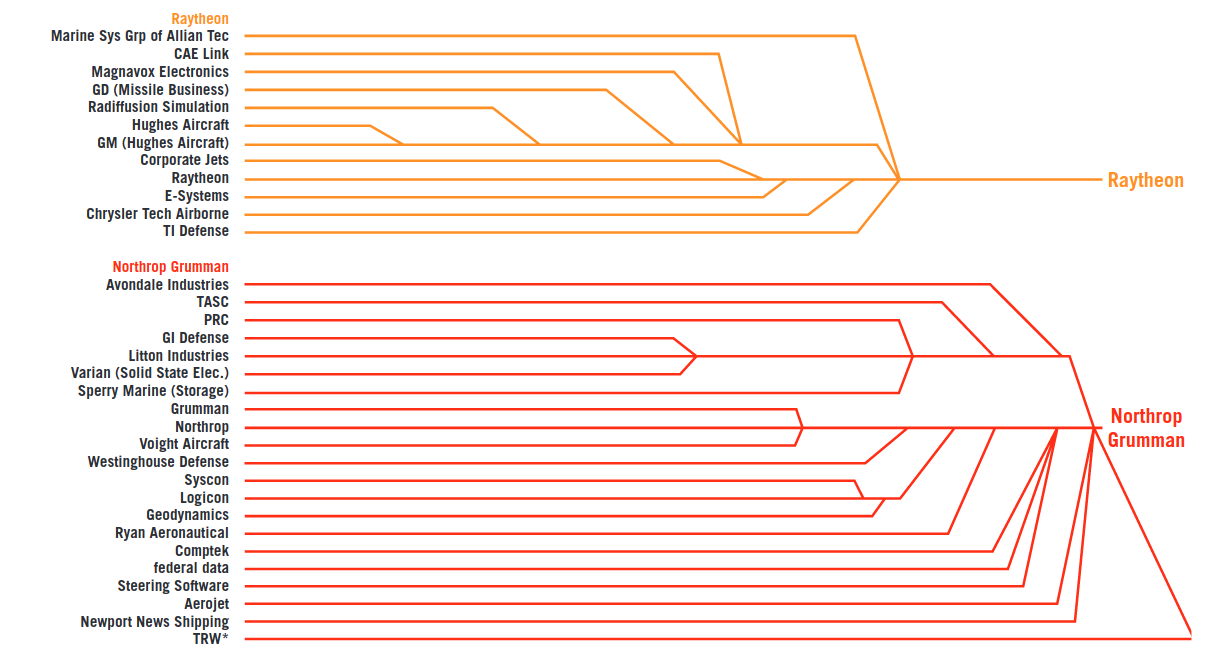

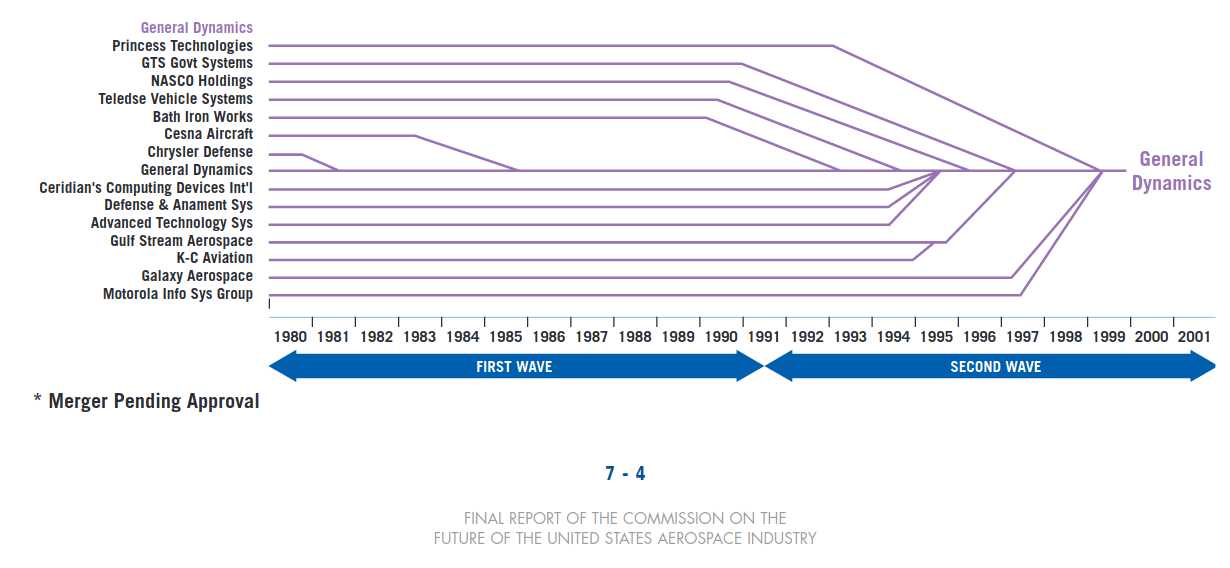

There is a lot to unpack here but I am going to highlight two things. One is the defense industry consolidation essentially into just 4 conglomerates, the other is top of mind for everyone interviewed is cyber attacks. In addition to my usual disclosures I should mention I work on a computer security product so I may be biased regarding the importance of cyber security.

“Just as old incumbent institutions with little to no organizational renewal impacted our ability to respond to COVID, the defense industry has undergone significant consolidation over the last 30 years. There has not been a new defense technology company of any scale to directly challenge these incumbents in many decades (SpaceX and Palantir are obviously sizeable ~20-year old “newer” entrants in adjacent areas).”

It is remarkable actually the degree of rollups and consolidation that the defense contractors have accomplished. Is this good for innovation? Most likely not. Monopolies while funding R&D generally are not incentivized to self disrupt in the Clayton Christensen sense of the word disruption.

Of these interviews there was tremendous attention given to cyber attacks:

“Elad: How should we think about that in the context of security at home? We've had a number of different ransomware attacks that have shut down oil pipelines that have shut down other core capabilities in the U.S.. How do you weigh those different challenges and how do you think the tech industry can get involved?

Katie:

...

I think that's so much in the cyber world operates similarly to nation state adversaries who operate in the gray space - they are getting away with so much because it's really hard to attribute who they are. It's hard to hold people to account whether it be criminally financially or just in the court of public opinion. When it comes to the cyber realm the hope is advanced technologies can help us respond and thwart threats more rapidly.”

“Elad: Where in particular do you think the U.S. is behind or on par? What sorts of technologies are capabilities?

Vincent: Recently we’ve seen a number of cyber attacks in the news. Many more similar attacks go unreported every year. At times, criminal hackers are extensions of their governments or are permitted to operate within their borders for a price. Our enemies don't have the limitations of laws and legal bureaucracies as we do. This enables them to move faster and act with plausible deniability.”

“Vincent: Getting back to cyber, there is no doubt we have a very fragile infrastructure, when it comes to our cyber backbone. There is risk in our control systems, water and power plants, and energy grid. The Colonial pipeline was turned off by some thugs using malware, sending the Northeast into chaos with long gas lines. Think about the vulnerabilities of hospitals, banks, and other critical services we take for granted. Go back to the California blackout from a few years ago. That was a mistake made by a single person that sent California into the dark for over 24 hours. That type of cyber attack in conjunction with military action somewhere in the world is most problematic. ”

“Elad: How has the nature of threats to our armed forces and national infrastructure shifted over the last decade?

Tina: Geographic distance and natural borders have provided nearly unbreachable defenses for the United States as a whole since its inception.

…

What has seemed to change is the relative ease of launching these attacks and their outsized impact - particularly through cyberwarfare. A recent example of this is the United Pipeline ransomware attack that brought gas lines to a standstill on the East Coast last month. The disruption of that incident is comparable to the scope of an airstrike. Which brings the overwhelming implications of strengthening our national security not only through our armed forces, but on the domestic “fence lines” of our cyber infrastructures and networks.”

Innovations in hardware for machine learning computation

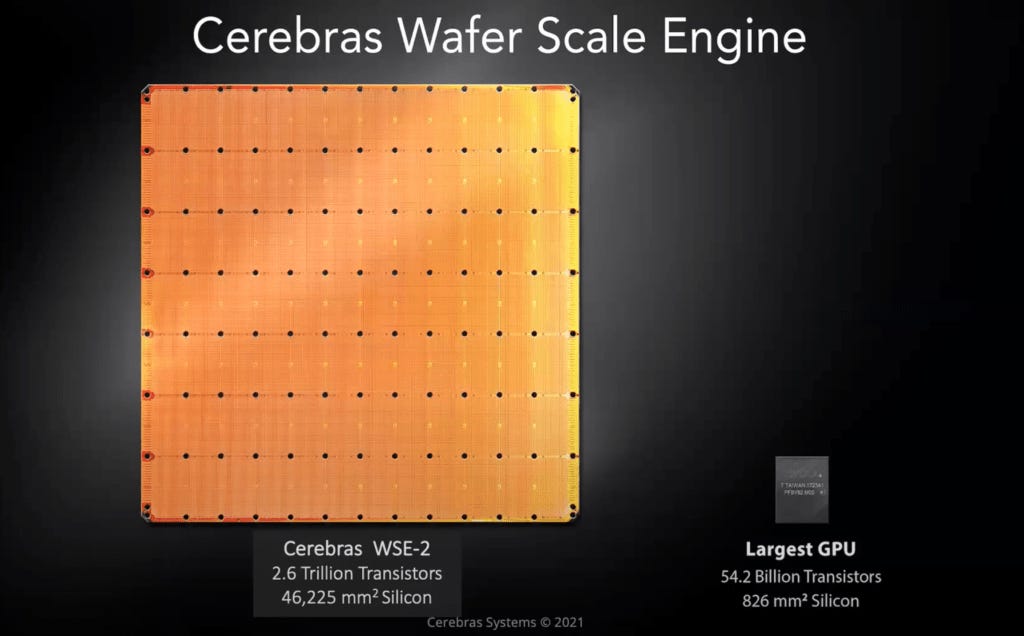

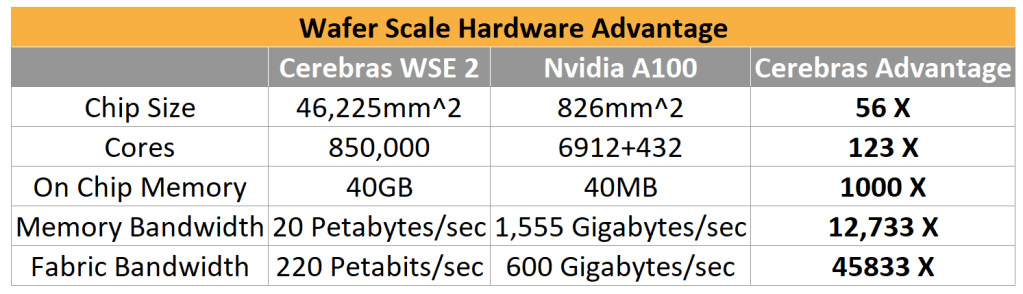

I found this article by Dylan Patel fascinating. Instead of chasing more transistors per mm^2 for a given chip size, why not just make a really big chip? It seems stupidly obvious as a potential way to scale compute power but as far as I know Cerebras has been fairly unique in pursuing this horizontal scaling of a single chip size.

Their goal appears to be direct competition with Nvidia based on their comparisons to the Nvidia A100:

“Semiconductor manufacturing has limited die size has been limited by the reticle limit for a long time. The reticle limit is 33x26 meaning that this is the largest size a lithography immersion stepper from ASML can pattern on a wafer. Nvidia’s largest chips are in the low 800mm^2 range mostly because going beyond this is impossible.

The Cerebras WSE is actually many chips on a wafer within the confines of the reticle limit. Instead of cutting the chips apart along the scribe lines between chips, they developed a method for cross die wires. These wires are patterned separately from the actual chips and allow the chips to connect to each other. In effect, the chip can scale beyond the reticle limits.”

The whole article was a very interesting read to me, worth going deep if you are an investor in the semiconductor space or interested in the implications of hardware accelerated machine learning. It is worth calling out the whole newsletter SemiAnalysis as being worth a subscription.

Also on my radar for machine learning hardware acceleration is custom analog chips.

From semiengineering.com:

““The digital AI ASIC might not be the ideal solution for IoT edge computing due to its high-power consumption and form factor,” says Hiroyuki Nagashima, U.S. general manager at Alchip. “Mixed-signal machine learning, inspired by nature like the human brain, should play an import role in the future world. Are we able to build a machine that can sense, compute and learn like human brain, and only consume several watts of power? It is quite a challenge, but scientists should aim to this direction.”

We already have some of the building blocks. “Analog-dot-product can make use of using analog filters, op-amps, etc.,” says Microchip’s Lee. “For example, you can compare two signals or mix them, and you can make a decision from the results. There are many cases that analog computation is much faster than digital computation.””

I do suspect that analog based machine learning will become commonplace by 2030 assuming of course they achieve the same compute results with significantly lower power consumption and heat output.

Like what you’re reading? Please share it with someone else who will enjoy it!

Intangible Value when Investing

Quotations from Intangible Value by Kai Wu

Here is the executive summary:

“Value investing has struggled over the past decade. We believe this is due to its failure to incorporate intangible assets, which play an increasingly crucial role in the modern economy. We consolidate our prior research to construct a firm-level measure of intangible value. We find that expanding intrinsic value to include intangibles can help restore value investing to its former glory.”

Kai used a natural language processing technique called topic clustering on his datasets to research individual companies and created “pillars” of what type of intangible value an investor is buying (if any) when purchasing these company’s stocks. He then sliced and diced these outputs to generate insights as well as find companies to backtest.

“The sections naturally fall into nine broad themes. The most central clusters form around the four intangible pillars: innovation, human capital, brands, and network effects. Five other research topics radiate out from this core.”

“Importantly, most of these metrics are scaled by price. Thus, they do not measure the total quantity of intangibles owned by a firm but instead quantify the share of intangibles we obtain by buying a fixed dollar amount of the firm’s equity. For example, we don’t care about how many total patents IBM has, but rather how many patents we obtain per dollar invested in IBM. Think of it like the “dividend yield,” except that instead of buying dividends, we buy patents.

Value investing is all about getting value for your money. Traditional valuation ratios measure the quantity of tangible assets obtained for a given dollar of investment. Our metrics are conceptually identical, except they focus on intangible sources of value (e.g., # patents, # PhD employees, $ brand equity per dollar invested). Our hope is that this metric helps us find efficient ways to obtain intangible assets.”

With that background let's look at some of the research.

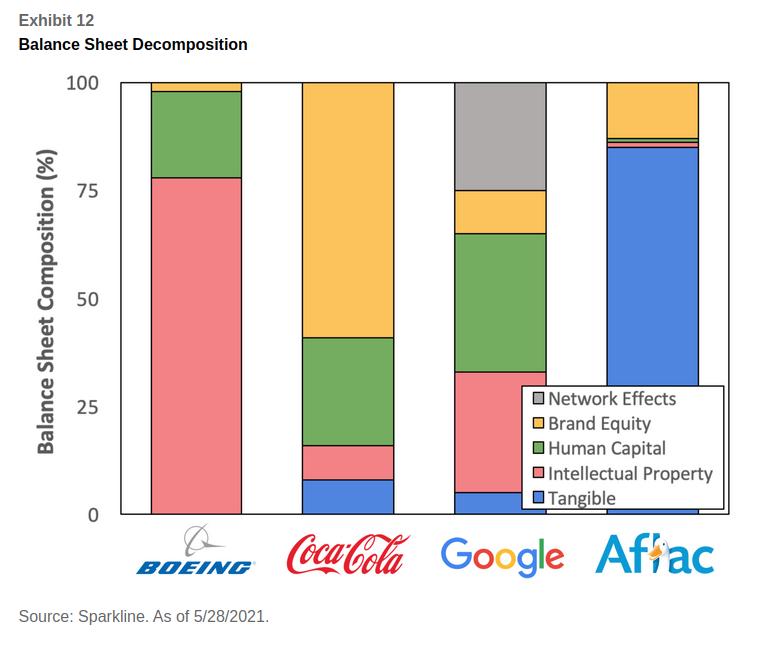

Notable Intangible Companies

Are some forms of intangible value more conducive to performance than others? As an investor should I be diversifying across different types of intangible values? Some interesting questions to consider if you buy into the premise of these intangible factors being quantifiable and represented by these buckets.

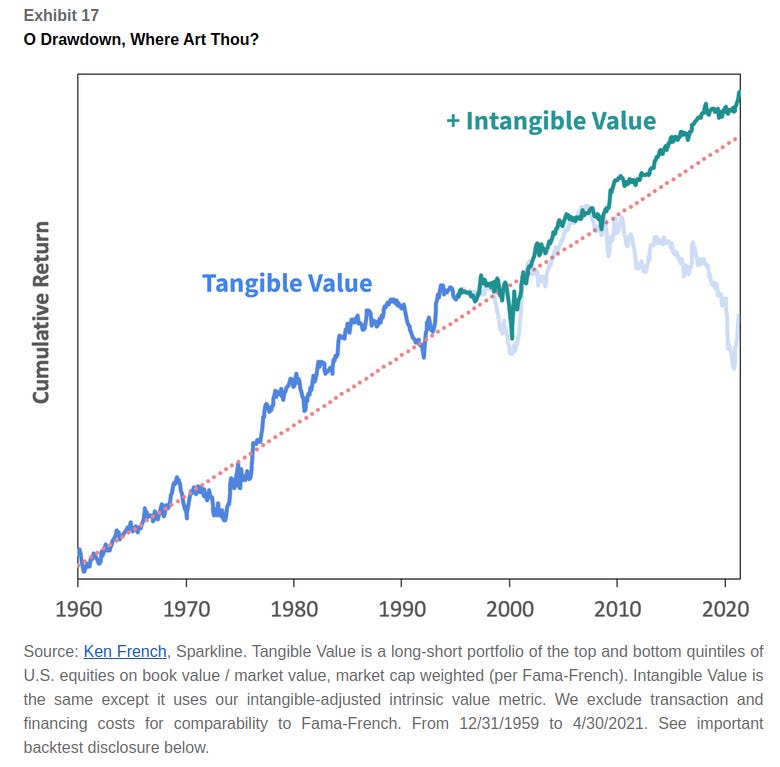

While academic in consideration Ken suggests that the value factor if expanded in definition to consider intangibles would not have had a post 2008 financial crisis drawdown and would continue to outperform through the 2010s.

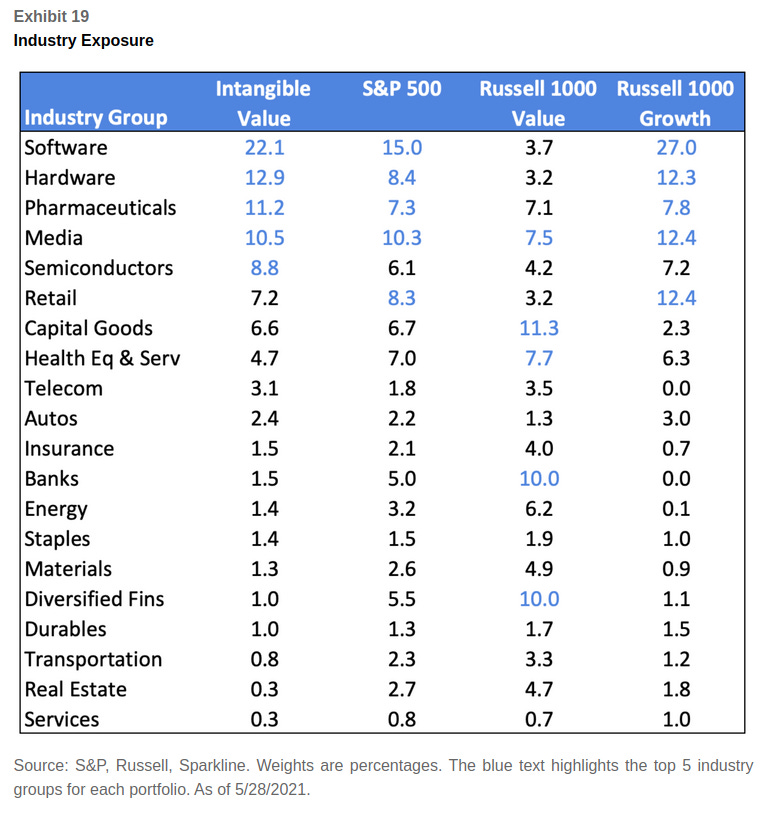

Where do these high intangible companies exist when looking at traditional sectors?

It would appear mostly in software, hardware, pharma (patents), media, and semiconductors none of which is surprising.

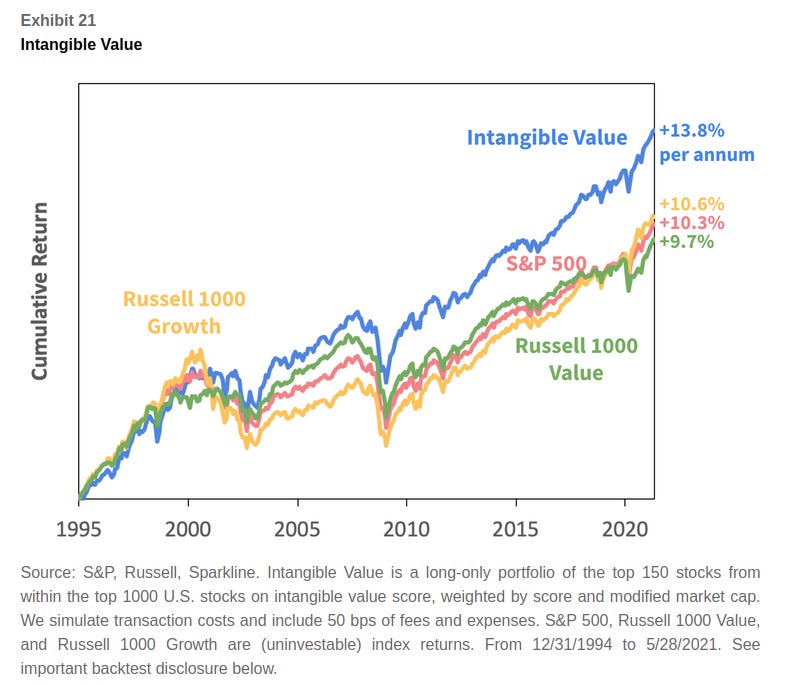

Kai backtests this concept to show it appears to outperform both value and growth style indices and the S&P500:

“We find that the Intangible Value portfolio would have outperformed the S&P 500. Interestingly, despite currently having factor exposures in between those of Russell 1000 Value and Growth, it would have also outperformed both.”

In my opinion Kai is finding companies that skilled qualitative investors traditionally find using some cleverly applied machine learning. He also has an ETF that focuses on these intangible factors. I look forward to his continued research.

If you want more (or less) link roundups vs long form articles please let me know in the comments.

Disclaimer

In no event will Prdctnomics or any of the Prdctnomics parties be liable to you, whether in contract or tort, for any direct, special, indirect, consequential, or incidental damages or any other damages of any kind even if Prdctnomics or any other such party has been advised of the possibility thereof.

The writer’s opinions are their own and do not constitute financial advice in any way whatsoever. Nothing published by Prdctnomics constitutes an investment recommendation, nor should any data or Content published by Prdctnomics be relied upon for any investment activities.

Prdctnomics strongly recommends that you perform your own independent research and/or speak with a qualified investment professional before making any financial decisions.